If you’ve ever felt overwhelmed comparing different online loan apps in the Philippines, Credy PH may seem like a simpler option.

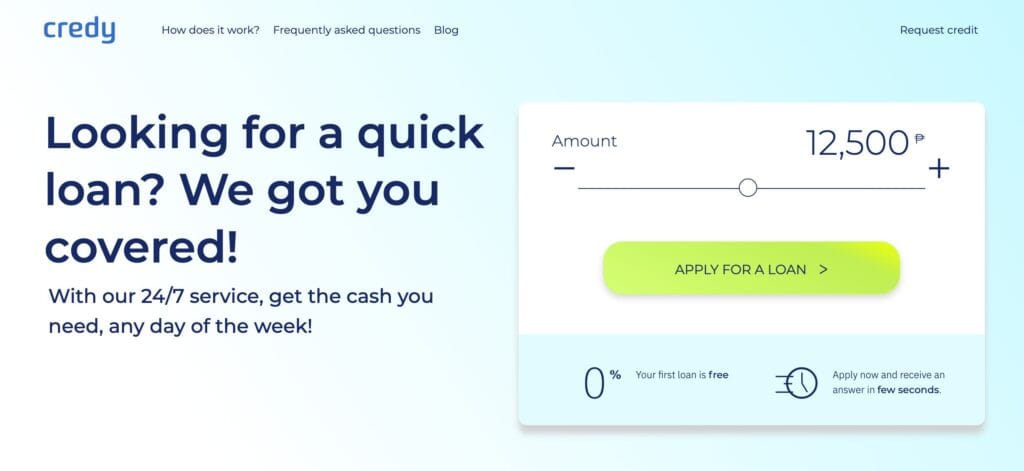

Instead of applying to several lenders one by one, Credy works as a loan comparison platform. You fill out one online application, and the platform helps you explore possible loan offers from partner financial institutions. Based on the official website, Credy shows loan offers from ₱1,000 to ₱25,000, with repayment periods from 61 to 120 days, and rates that can range from 0% up to a maximum APR of 143%, depending on the lender and borrower profile.

That makes Credy different from apps like MoneyCat, Finbro, or Cash Express, which are typically reviewed as direct lending platforms. With Credy, the main value is not “instant approval from one lender,” but rather a faster way to compare multiple loan options in one place.

So, is it legit? Is it useful? And is it actually worth trying for Filipino borrowers?

In this review, we’ll look at how Credy PH works, what type of borrower it may suit, and why it may be better viewed as an alternative to direct loan apps, rather than a direct lender itself.

Quick Summary

Credy PH is not a direct lender. It is a loan comparison platform that helps borrowers in the Philippines explore offers from partner lenders through one online application.

That distinction is important.

Credy itself clearly states that it does not provide loans, does not act as a financial institution, and does not participate in the loan agreement process. In simple terms, it’s best understood as a comparison platform for online loan offers, not a typical online loan app.

What Credy PH publicly shows on its official website

- Loan amount: ₱1,000 to ₱25,000

- Loan term: 61 to 120 days

- APR range: 0% to 143% maximum APR

- Example shown: A ₱1,000 loan at 36% annual interest over 3 months would have a total repayment of ₱1,090

- Main benefit: One application can help you compare multiple lender offers instead of applying separately.

Short verdict

If you want a faster way to compare online loan offers, Credy can be a practical option. But if you prefer the clarity of dealing directly with one lender from the start, a direct lending app may still be the better fit.

Credy PH at a Glance (2026)

A quick overview of how Credy PH works as a loan comparison platform for borrowers in the Philippines.

| Platform Name | Credy Philippines |

|---|---|

| Official Website | credy.ph |

| Service Type | Loan comparison platform |

| Direct Lender? | No |

| Publicly Shown Loan Range | ₱1,000 to ₱25,000 |

| Loan Term | 61 to 120 days |

| Interest / APR | 0% up to 143% APR (varies by lender) |

| Sample Cost Shown | ₱1,000 loan, 36% annual interest, 3 months = ₱1,090 total repayment |

| Main Process | One form, compare offers from partner lenders |

| Best For | Borrowers who want to compare online loan offers faster |

What is Credy PH?

Credy PH is an online platform that helps borrowers in the Philippines compare possible loan offers from multiple financial institutions.

Instead of applying directly to one lender, you submit your details through Credy, and the platform tries to show you available offers based on your requested amount, repayment period, and profile.

That makes Credy best described as:

- a loan comparison platform

- a platform for comparing online loan offers

- a tool for exploring multiple lender options

- a starting point before choosing a lender

It is not the same as a traditional online lender that directly approves and releases funds.

This matters because many borrowers in the Philippines are already familiar with direct loan apps. But with Credy, the platform’s main purpose is different:

It helps you save time by checking multiple possible loan offers in one place.

That can be genuinely useful if you:

- don’t want to fill out multiple forms manually,

- want to compare options faster,

- or are still deciding which lender may suit you best.

Credy PH is not a direct lender (and why that matters)

This is the most important thing to understand before using Credy.

According to its official website, Credy explicitly states:

- it does not provide loans

- it does not act as a financial institution

- it does not participate in the loan agreement process

- the platform is strictly informational

- displayed calculations are illustrative only

Why this matters for borrowers

If you use a direct lender:

- the lender itself sets the terms

- the lender approves or rejects you

- the lender disburses the funds

- the lender handles collections and repayment terms

If you use Credy:

- Credy helps you compare loan offers

- the partner lender makes the actual decision

- the partner lender sets the final interest, fees, and contract terms

- the partner lender becomes the company you are legally dealing with

Practical takeaway

Think of Credy as a comparison platform, not the final loan provider.

That means the safest way to use it is:

- Compare the available options

- Check who the actual lender is

- Review the lender’s legal disclosures and repayment terms

- Only accept an offer if the total repayment makes sense for your budget

That’s a much more realistic and responsible way to approach platforms like this in the Philippine online loan space.

Is Credy PH legit?

Yes — Credy PH appears to be a real and functioning loan comparison platform, and its website is actually more transparent than many suspicious online loan pages.

Why?

Because it clearly tells users that it is not a lender, and it openly shows the basic loan range, repayment term, and maximum APR on the homepage. It also identifies itself as a brand of Traffic Control OÜ, an Estonia-registered company, with a listed address in Tallinn, Estonia. (credy.ph)

But here’s the honest answer

Credy being “legit” does not automatically mean every partner offer is automatically the best or safest choice.

Since Credy is only the comparison platform, the real risk and real legal relationship sit with the final lender.

So if you want to assess safety properly, you should always verify:

- the actual lender name

- whether the lender is properly registered / authorized

- the full disclosure statement

- the exact repayment schedule

- penalties for late payment

- whether the lender asks for suspicious upfront fees (red flag)

Simple rule

Credy itself can be legitimate as a comparison platform, but you should still evaluate the lender behind the final offer.

That’s the right way to explain it in a Philippine borrower context.

How much can you borrow with Credy PH?

According to the official website, Credy shows loan offers from ₱1,000 to ₱25,000.

That makes it suitable for:

- small emergency borrowing

- short-term cash gaps

- basic bills or urgent personal expenses

- borrowers looking for microloan to mid-small loan options

Realistic expectation for first-time borrowers

Like most online loan ecosystems in the Philippines, the maximum amount shown on a platform is usually the highest possible offer, not a guaranteed first-time approval.

So if you’re new to online borrowing, it’s safer to assume:

- your first offer may be closer to the lower end

- approval depends on the partner lender

- some lenders may be stricter than others

- your income, ID verification, and risk profile matter

Practical advice

Instead of assuming you’ll get ₱25,000 immediately, a more realistic expectation is:

Credy may show offers up to ₱25,000, but first-time borrowers should expect smaller approved amounts depending on the lender and their profile.

That’s normal in this market.

Loan term and repayment period

Credy shows a repayment period of 61 to 120 days on its official website.

That’s a fairly common range for short-term online borrowing in the Philippines.

Why this can be a positive

Compared with ultra-short payday loans that are due in 7 to 30 days, a 61 to 120 day window may feel more manageable for some borrowers.

It can help if you:

- need a bit more breathing room,

- want to avoid next-payday pressure,

- or prefer a short-term loan that is not due immediately.

But don’t assume longer = cheaper

A longer term only helps if:

- the repayment schedule is clear,

- the total cost is still reasonable,

- and the lender isn’t stacking high fees.

So always check:

- total amount payable

- number of payments

- exact due dates

- late fees

- whether the loan is installment-based or lump-sum

That’s more important than the number of days alone.

Interest, APR, and real cost of borrowing

This is where borrowers need to pay close attention.

Credy states that partner lenders may offer rates from 0% up to a maximum APR of 143%. The platform also shows a representative example:

- Loan amount: ₱2,000

- Annual interest: 36%

- Repayment term: 3 months

- Total repayment after 3 months: ₱2,180

Quick explanation:

- Annual interest rate: 36%

- 3 months = 1/4 of a year

- Interest = ₱2,000 × 36% × 3/12 = ₱180

- Total repayment = ₱2,180

What this means in practice

The sample cost shown is fairly understandable, but it is still only an example.

Credy itself also says that the displayed calculations are illustrative and that users should check the official websites of the actual lenders for precise terms.

Most important takeaway

Because Credy is a comparison platform:

- the actual lender decides the final rate

- the actual lender decides the final fees

- the actual lender decides the real repayment schedule

So even though Credy shows “up to 143% APR,” your actual offer may be:

- lower,

- similar,

- or in some cases still expensive enough to require caution.

Best borrower habit

Before accepting any offer, ask these questions:

- How much money will I actually receive?

- How much will I repay in total?

- Are there processing or service fees?

- Are there penalties for late payment?

- Can I repay early, and if yes, is there any fee?

If you don’t know those answers yet, don’t rush into the loan.

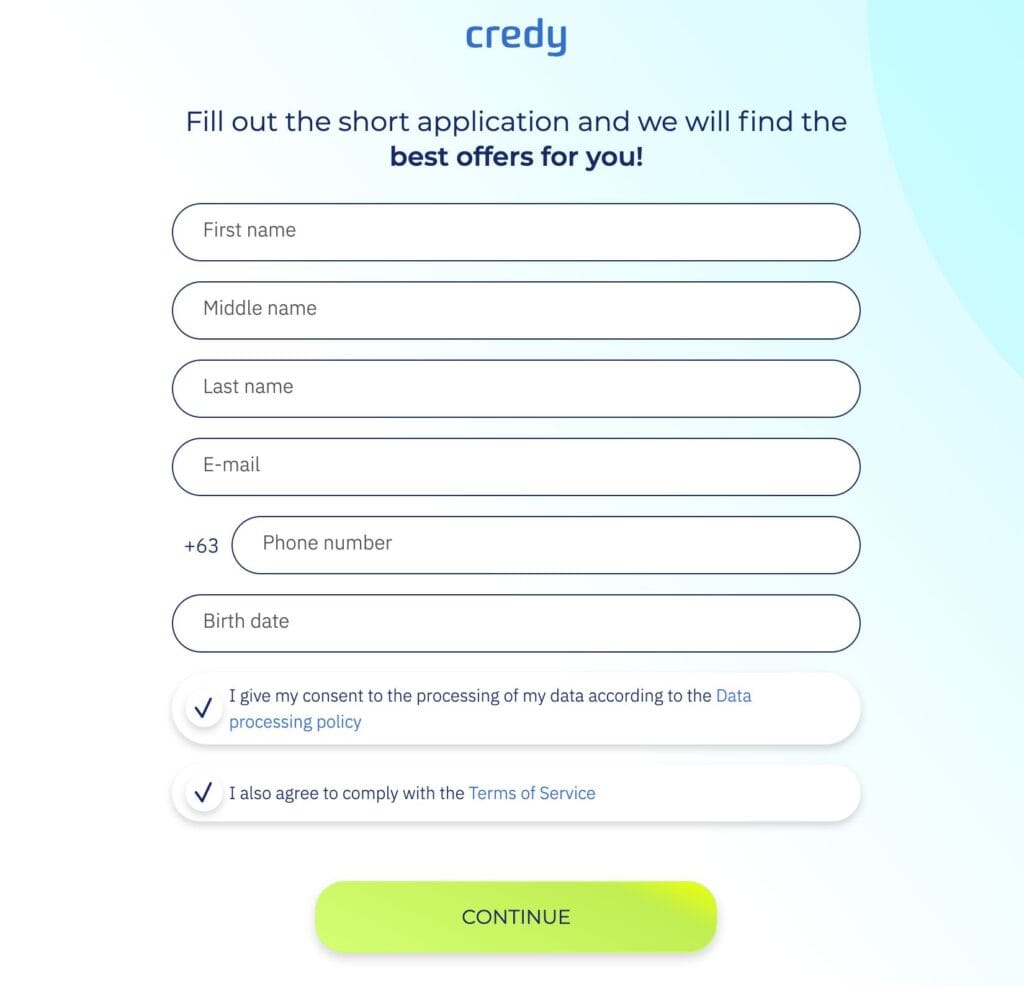

How does Credy PH work?

Credy is designed to make the comparison process simple.

Based on the platform’s public flow, the process generally works like this:

- Visit Credy.ph

- Select the amount you want to borrow

- Choose your preferred repayment period

- Fill out the online application

- Review possible offers shown on the platform

- Choose the offer that fits your needs

- Complete identity verification

- Receive funds if approved by the lender

Why this appeals to many borrowers

Instead of applying to multiple apps one by one, you can potentially:

- save time,

- compare several options,

- and avoid guessing which lender to try first.

But here’s the realistic version

The comparison step may be fast.

The final approval and disbursement still depend on the lender you choose.

So the best way to explain it is:

Credy may help you find possible loan offers faster, but the final loan decision is still made by the partner lender.

That’s the most accurate way to understand the platform.

Who should consider Credy PH?

Credy PH is not for everyone — but it can be a smart option for the right borrower.

Credy may be a good fit if you:

- want to compare loan offers before choosing

- don’t want to apply to multiple loan apps manually

- are still exploring which lender may suit you

- prefer a comparison-first approach

- want a practical alternative to direct loan apps

Credy may be less ideal if you:

- already know which lender you trust

- want the clearest terms upfront from one company

- prefer dealing directly with one lender from the start

- need a guaranteed same-day cash solution from a specific app

- don’t want the extra step of reviewing third-party lender terms

In short:

Credy is best for borrowers who want to compare first, not for borrowers who want one direct lender immediately.

Credy PH vs direct loan apps in the Philippines

This is where Credy becomes much easier to understand.

Credy PH (loan comparison platform)

Best for:

- comparing multiple offers faster

- exploring options before deciding

- avoiding multiple manual applications

- borrowers who want a broader view of what may be available

Main trade-off:

- you still need to evaluate the actual lender behind the offer

Direct loan apps / lenders

Examples often reviewed by Filipino borrowers include direct lenders like:

Best for:

- borrowers who already know which platform they want

- clearer lender identity from the start

- more predictable product structure

- users who prefer dealing directly with one company

Main trade-off:

- you may need to compare several apps manually if you want the best option

Simple comparison

If you’re asking:

- “Which lender should I use?” → a direct lender review may help more

- “What options might I have?” → Credy may be the better starting point

That’s why Credy works better as an alternative option rather than a “top lender” type of review.

Pros and Cons of Credy PH

A quick look at the main strengths and possible drawbacks of using Credy PH as a loan comparison platform in the Philippines.

Pros

- One application can help you compare multiple loan offers

- Useful for borrowers who do not want to apply app by app

- Clearly explains that it is not a direct lender

- Shows the basic loan range, term, and APR on the website

- Can save time when comparing online loan options

- Works well as a starting point before choosing a lender

Cons

- Credy PH is not a direct lender

- The final loan terms depend on third-party lenders

- The maximum advertised amount may not reflect first-time approvals

- APR can still be high depending on the lender

- Borrowers still need to verify the actual lender carefully

- Some users may expect direct approval from Credy itself

Is Credy PH worth trying?

For the right type of borrower, yes.

Credy PH is worth trying if:

- you want a faster way to compare online loan offers,

- you’re tired of jumping from one loan app to another,

- you want to explore multiple options before committing,

- and you’re willing to review the final lender carefully.

Credy PH may not be the best fit if:

- you want a direct lender with clear terms immediately,

- you already know which app you trust,

- or you’re likely to accept the first offer without reading the full details.

My honest take

Credy is best understood as:

a practical loan comparison platform and a useful alternative to applying with multiple direct loan apps one by one.

That’s a much stronger and more accurate positioning than trying to treat it like a lender review.

It’s not “the loan.”

It’s the platform that helps you compare the loan options.

And that’s exactly why some borrowers may actually find it useful.

Final Verdict

Credy PH is a reasonable option for Filipino borrowers who want to compare possible online loan offers faster instead of applying to multiple loan apps separately.

Its biggest strength is convenience:

- one application,

- multiple possible offers,

- less guesswork about where to start.

Its biggest limitation is also obvious:

- it is not the lender,

- so the actual experience depends on the partner lender you finally choose.

Frequently Asked Questions About Credy PH

Here are some common questions borrowers in the Philippines may have before using Credy PH as a loan comparison platform.

1. Is Credy PH a direct lender?

No. Credy PH is not a direct lender. It works as a loan comparison platform that helps borrowers in the Philippines compare possible loan offers from partner financial institutions.

2. How much can I borrow through Credy PH?

According to the official website, Credy PH shows loan offers ranging from ₱1,000 to ₱25,000. The final approved amount depends on the partner lender and your eligibility profile.

3. What is the repayment period on Credy PH?

Credy PH publicly shows repayment terms from 61 to 120 days. However, the final repayment schedule still depends on the lender behind the offer you choose.

4. What is the maximum APR shown on Credy PH?

The platform states that partner lender rates can range from 0% up to a maximum APR of 143%, depending on the lender and borrower profile.

5. Is Credy PH worth trying?

Credy PH can be worth trying if you want a faster way to compare online loan offers in one place. It is especially useful for borrowers who want to explore options before choosing a direct lender.